The Hidden Tax Trap of 401(k) Withdrawals

Withdrawing money early from your 401(k) is usually a financial disaster. Once you add federal tax, the 10% penalty, and Massachusetts state tax, the real tax hit is often 37% or more. Before you tap into your retirement to buy a home or pay off debt, read this first.

Why I’m Writing This

In all my years as a tax attorney in Lowell, I have sent one mass email to my entire client list.

It wasn’t a holiday message.

It wasn’t a newsletter.

It was this warning.

Why? Because I keep seeing good, hardworking people destroy their long-term wealth after getting bad advice from an HR department or a 1-800 customer service line.

The conversation is always the same.

A client sits across from me in April.

I tell them they owe thousands in taxes.

They look shocked and say:

“But I already took the tax out. The lady on the phone said they withheld 20%.”

I hate delivering that news.

So let me explain it now — while you can still avoid the damage.

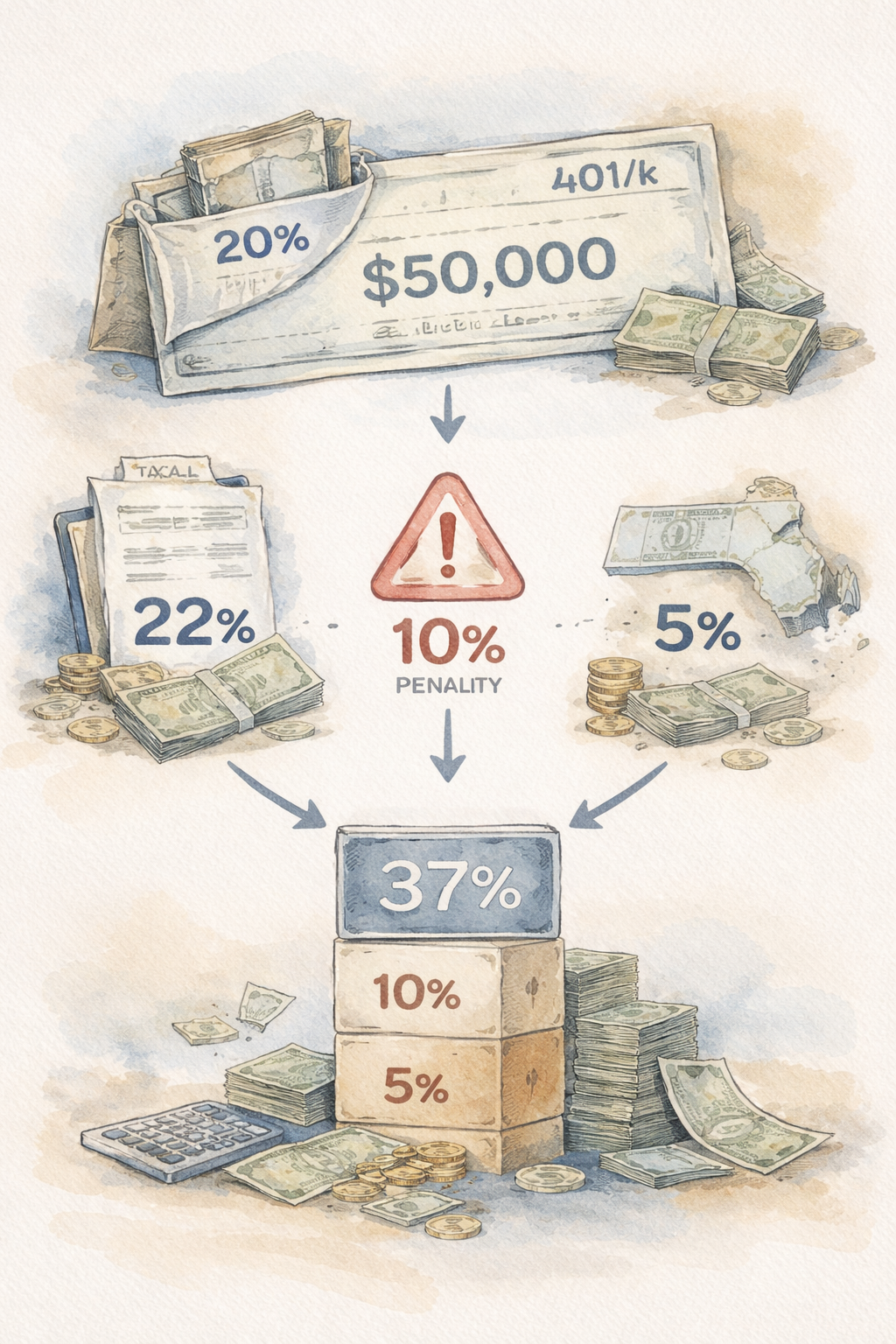

1. The Big Myth: “The 20% Withholding Covers It”

When you take an early 401(k) withdrawal, the plan administrator is required to withhold 20% for federal taxes.

Most people think that means:

“Taxes paid. Done.”

It is not done.

That 20% is just a down payment.

Here’s what’s missing:

Federal Income Tax

If you’re still working, adding a $50,000 withdrawal on top of your salary often pushes you into the 22% or 24% tax bracket. You’re already short.

The 10% Early Withdrawal Penalty

Unless you meet a very narrow exception, you owe this penalty — and the 20% withholding does not cover it.

The Massachusetts Surprise

Most 401(k) companies withhold nothing for Massachusetts.

Massachusetts still wants its 5%.

The Real Math

22% Federal tax

10% Penalty

5% Massachusetts tax

= 37% total tax rate (often higher)

They withheld 20%.

You owe around 37%.

Come April, I’m the one who has to tell you about the gap.

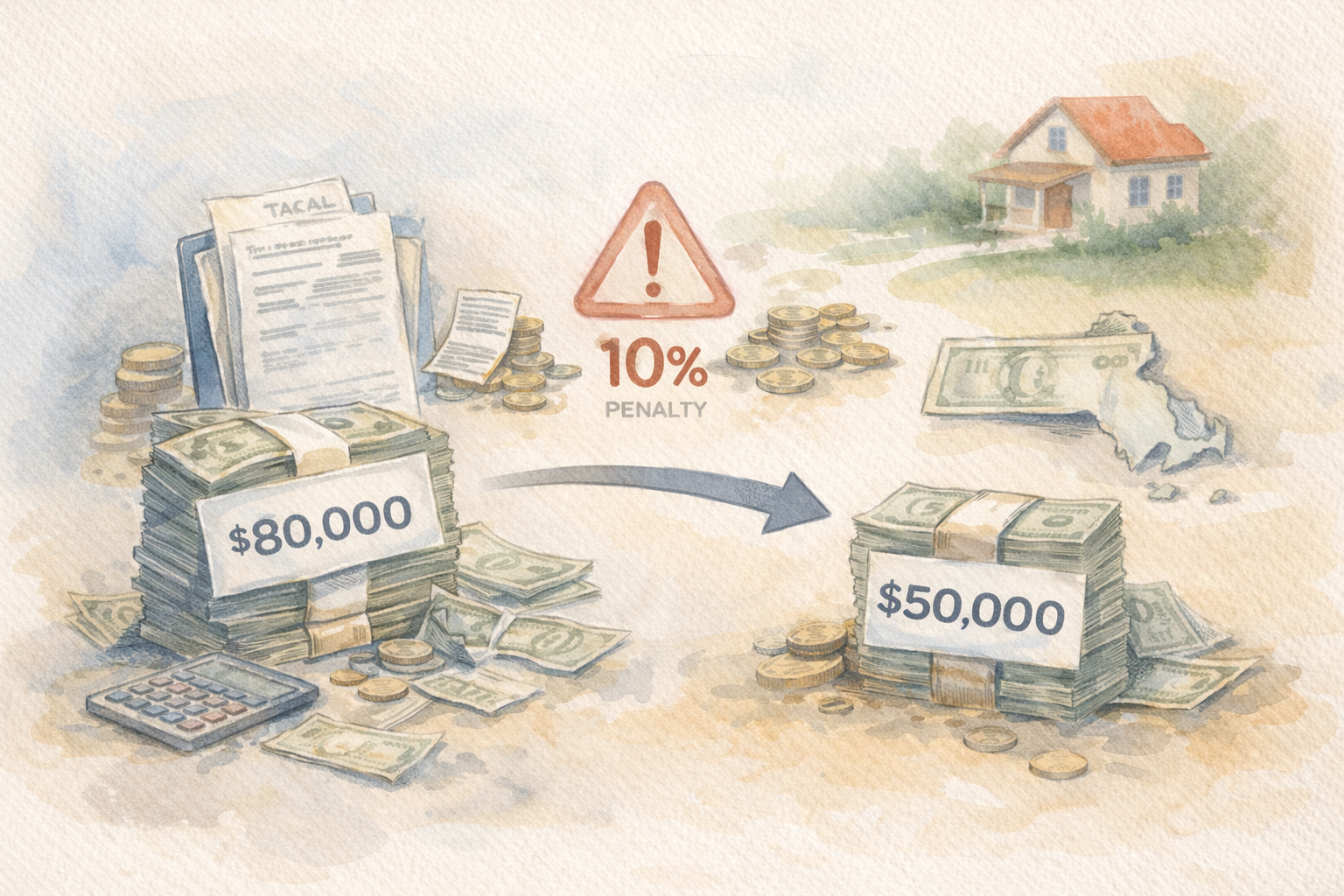

2. The Down Payment Disaster

($80,000 Gone to Get $50,000)

I see this constantly.

A young couple wants to buy a home in the Merrimack Valley.

They need $50,000 for a down payment.

They withdraw $50,000 from their 401(k).

Here’s what happens:

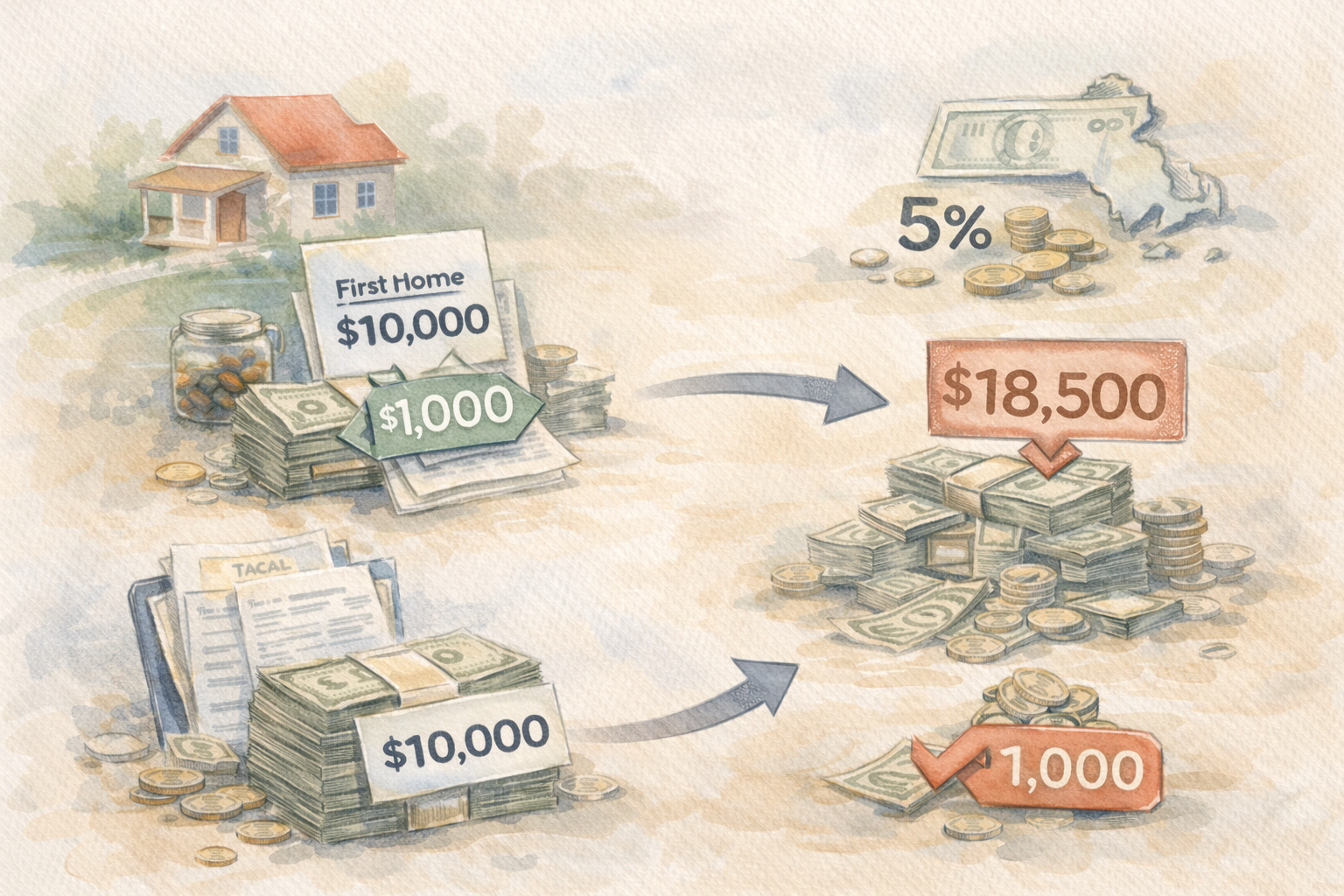

Taxes and penalties come to roughly $18,500

To actually net $50,000 in cash, they have to withdraw close to $80,000

That’s $80,000 of hard-earned retirement savings gone — instantly.

Retirement planners hate this.

And for good reason: you’re burning decades of compounded growth just to get cash today.

A Smarter Alternative: The “Dad Loan”

I once ran these numbers with a young client and his father.

When the father realized his son was about to lose $30,000 just to access his own money, he immediately offered a small family loan to bridge the gap.

The son hadn’t asked because asking family for help feels uncomfortable.

Withdrawing from a 401(k) feels “easy.”

Don’t do the easy thing.

Do the smart thing.

3. The “First-Time Homebuyer” Myth

This one drives me crazy.

Many people believe that withdrawing from a 401(k) to buy their first home is tax-free.

It is not.

You still owe income tax.

Some people think it’s at least penalty-free.

Also not true.

There is a first-time homebuyer penalty exception — but it’s capped at $10,000.

That saves you $1,000.

Nothing wrong with saving $1,000.

But when the total tax bill is $18,500, that’s not exactly a great deal.

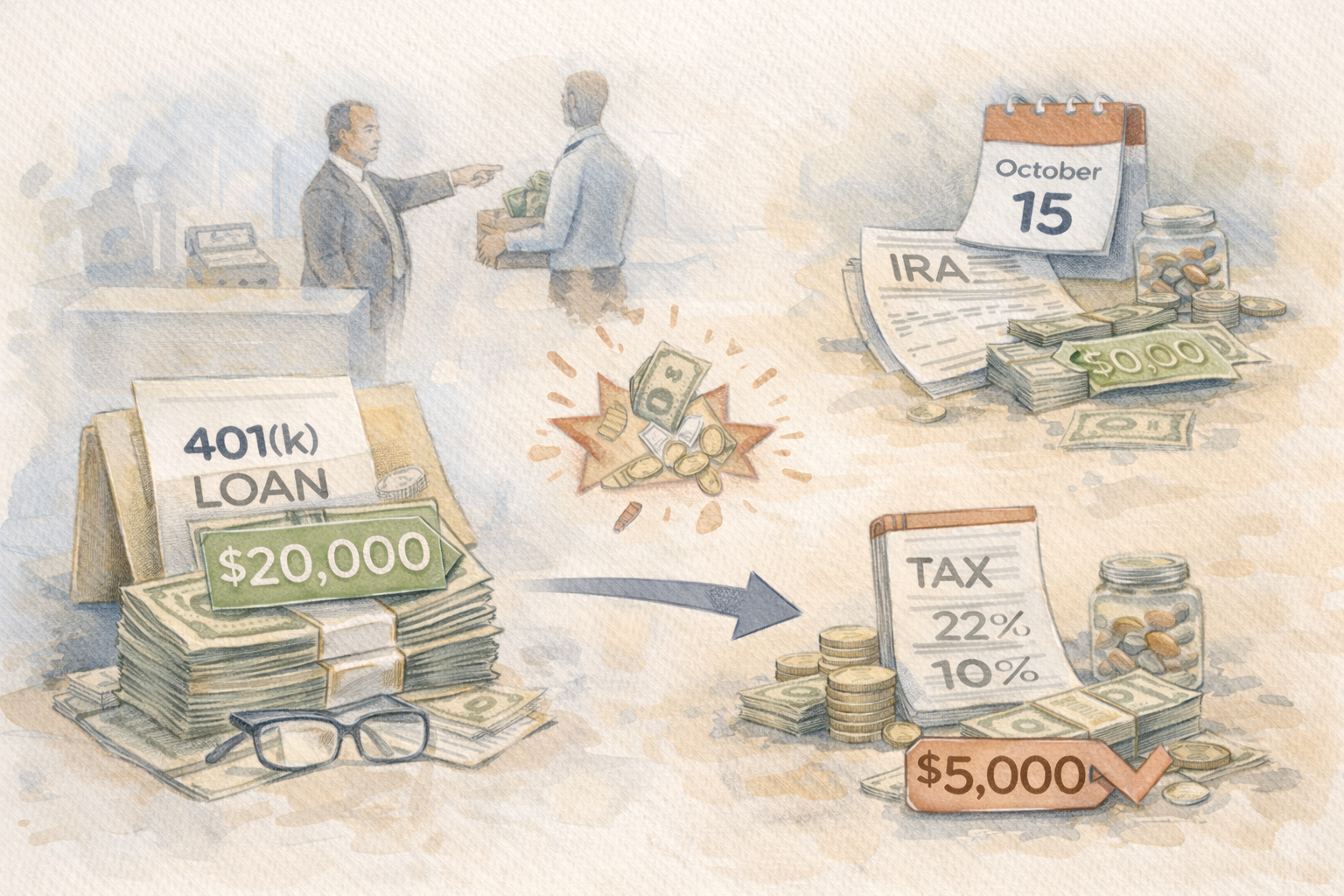

4. The Job-Change Trap

When a 401(k) Loan Explodes 💣

Many people try to be smart and take a 401(k) loan instead of a withdrawal.

That can be a good strategy — until you leave your job.

If you quit or get fired, the loan often becomes due almost immediately.

If you can’t repay it, the entire balance turns into a taxable distribution 💥

That means:

Income tax

Possible penalties

A surprise bill you weren’t planning for

The October 15th Escape Hatch 🗓️

If this happened to you, don’t panic.

You still have time to fix it. It is called a “Qualified Plan Loan Offset” (QPLO ) Roll Over IRA.

If you left your job in 2026, you generally have until October 15, 2027 ( the tax filing extension deadline) to roll over the loan offset amount into an IRA.

The Key Point Most People Miss ❗

This is not an all-or-nothing situation.

If your loan was $20,000 and you can only come up with $5,000, deposit the $5,000.

✅ You avoid taxes and penalties on that portion.

Every dollar you roll over reduces the damage.

I’ve seen clients save thousands of dollars by scraping together even a small amount once they understood the math. For example, if you live in Massachusetts, are under the age of 59 ½ and are in the 22% tax bracket, just depositing ½ of the $20,000 loan offset, which saves a taxpayer $3,700. In the $ 5,000 example I gave, the tax savings would be $ 1,850.